If you’ve worked in business, healthcare, ministry or almost any corporate entity in the last generation, chances are good you’ve taken a personality test – perhaps even a few. You found out you’re an ENFP or an INTJ or an Otter/Lion, or a Steady Wing 2 who needs to focus on your Bright Side. These tests tell you how you digest information, how you play with others and often things you didn’t know about yourself.

Your tax refund, and your response to it, can be a similar litmus test for what kind of investor you are. The way money stays with and returns to us – and how we use it when we get it – says quite a bit about us. Your tax return can tell you if there are habits and plans you need to change, or if what you’re doing with it works for you.

Consider a few examples:

- Jon Vacation – Receives his tax return all at once, usually by early April. He always uses the money to pay for his family’s summer trip.

- Jane Breakeven – Sets up her taxes so she gets the money through the whole year and invests it. Even if she ends up owing a little at the end of the year, she keeps the interest she made.

- Joe NoPlan – Gets his taxes done right around midnight every year on April 15, and uses his refund (if he gets one) on the most pressing bills or impulse purchases.

These profiles just tell us about Jon, Jane and Joe, and that’s it – they don’t say anything about whether their decisions are bad, good, wise or foolish. Their wishes about what would happen tell us about their investor personalities (Jon wants to be in a lower bracket, Jane secretly would love to have a little extra scratch every spring).

In that way, a tax refund can act as a shorthand personality test for what kind of investor you are. If yours isn’t matching up with who you are, here are four ways to get closer to where you want to be.

1. An Important Tool

You ever get to the end of the year and have absolutely no idea how much you should be expecting in your refund, or even if you’ll get one at all? The IRS Withholding calculator can save you a lot of time and headaches, whether you’re a Jon, Jane or Joe. This fairly simple tool will give you a pretty good idea of what to expect so you can plan accordingly.

2. The Changing Tide

The Tax Cuts and Jobs Act of 2017 changed things for everyone. The brackets are different, the process is different and the ripple out will be felt for a long time. Visits to the IRS website are up by 10 percent this year because people have so many questions about how things work now.

One of the biggest changes for many of us is the standard deduction of $24,000 for the designation “married filing jointly” – up from $12,700 in previous years. Itemizing no longer makes sense for much of the US population – one estimate put it at 30 million fewer people itemizing this year. Most of the Jons, Janes and Joes out there will take this deduction, which can simplify the process for much of the population.

3. W-4 Us or Against Us

If you go through the IRS withholding calculator, you’ll notice several links on your results page that take you to your W-4, where you can make adjustments if you’re surprised by your refund (or lack thereof). Your W-4 is where your refund takes the shape you want it to.

One recent issue is that employers have changed withholding numbers and tax status, and employees haven’t. So your employer is ready for the new brackets and prepared their taxes accordingly, but you end up with less of a check than you thought, which can be a huge problem if you – talking to you, Joe Public – are counting on that cash for bills and high-interest debts. Adjusting your W-4 isn’t as complex as you might think, and the IRS calculator will take you right there.

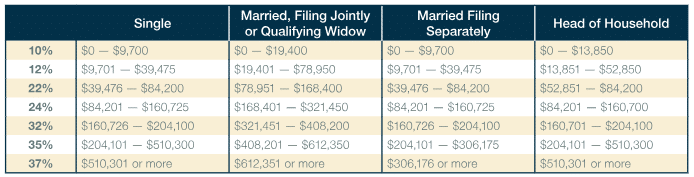

4. The Current Brackets

This bracket may not be as exciting as the March Madness or Master’s Golf bracket on the fridge at work, but its impact will be felt deeper and longer:

As with most things like this, we usually find ourselves somewhere in the middle, and then somewhere in the middle of that middle. The American population is an obvious bell curve, and the brackets are fairly wide. But you may find yourself on the edge of one of these brackets, especially after a life event like selling a business or getting an inheritance or promotion. That’s when it’s essential to know your brackets.

If you are close to the edge of a bracket, the math is simple: that extra bump in income could cost you an extra 2 or 3 percent in taxes, which could mean taking a bigger hit than the bump added.

Fortunately, reducing your taxable income isn’t rocket science.

Let’s go back to our people:

- Jon – Puts a few grand extra in his HSA every year, and therefore gets himself just below the line to be in the 32 percent bracket.

- Jane – Keeps careful records of her donations and adjusts accordingly every year to keep herself in a lower bracket. This is considered a Qualified Charitable Deduction.

- Joe – Has almost no idea what bracket he’s in, but occasionally gets lucky and contributes enough into his 401(k) that his tax bill is lower. Not this year, though.

Soon enough, all of these folks will retire, and then the conversation becomes more complex. After 70.5 years of age, Required Minimum Distributions start coming out of your retirement accounts, and can change your taxable income. Jane, of course, has a plan for this and will donate her RMDs immediately when they come through. Jon’s not sure what he’s going to do, and Joe hasn’t even thought of it yet.

Know your brackets!

That’s probably the advice you’ll get the most traction out of as the tax landscape changes with the political one. Know your brackets and know yourself. A beefy tax return doesn’t mean much if you’re hurting financially through the rest of year; a low tax refund could be a big problem if you thought you’d have money to pay off some pressing bills. That depends on your plan, and that depends on you.

A solid financial advisor can make all the difference when it comes to strategizing for taxes that fit your life and planning for major life events. Jon, Jane and Joe (especially) can all use someone to help them strategize and position their portfolio to make and keep the most in the years to come.

How can we help you? Our advisors are here to make the complex simple and put your financial needs and interests first, whether you’re a Jon, Jane, or even a Joe.

This article is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate professional should be sought.