I was standing in the middle of a sports bar with my coworkers when I saw him. He was sitting with a friend, relaxing and enjoying a beer. I just had to run over and greet him!

He quickly exclaimed: “I got a new job!” I jumped at the news and give him a big hug. But to understand the excitement, we have to back up a bit.

I had first met him and his family a few months back. He’s in his late 60s, but you would never have guessed it – there’s an abundant energy and youth about him. In that initial meeting, he stated that he would never retire.

He had a great career and a beautiful family. He was saving into his 401(k) and the majority of his money was tax deferred. He and his wife had done a fantastic job helping their kids pay for school and had saved into 529 plans.

This family came to us at the beginning of the year seeking help in creating a financial plan. One of the major gaps in the plan was the vast majority of his savings and investments where in tax-deferred accounts through employer retirement plans. They didn’t have access to money in the most financially valuable way in case they ever faced a financial bind.

Sure enough, we were still in the discovery phase when we got the phone call. He had been laid off. And even with a great severance package, I could tell he was worried.

For the next few months, we met to continue his plan. He would talk about the job search, the numerous interviews, and the worry. When you are looking for jobs at a certain level of income, companies take their time. And since my client had most of his money in a retirement plan, he would have to pay taxes to withdraw.

That leads us back to the bar. I was so pleased to hear his story ended happily and that he wouldn’t need to access his retirement dollars. But it’s also a reminder of why I enjoy being a financial advisor.

I see this type of skewed proportion often. It’s key to understand how to save for retirement so that you have money available when you need it, not just when you plan on needing it. In addition, we need to plan for life outside of retirement. Investing should have financial accumulation goals in all stages of life.

(These results are for illustrative purposes only and should not be deemed a representation of future results. Circumstances, solutions, and/or results are based on specific facts tied to unique client situations. Favorable results cannot be guaranteed even in a similar scenario. Each specific set of circumstances will differ depending on client needs and profile. Actual results may be more or may be less than those shown. Past performance does not guarantee future results. This assessment is that of the writer, and not the recommendations or responsibility of Cetera Advisor Networks LLC or its representatives. The solutions presented in this scenario are being offered through CWM, LLC.)

The Prep Work

Before I can teach clients to save for retirement and financial accumulation, first I guide them through how to organize their money.

We discuss spending money and saving money. We identify goals and analyze spending (and create a budget if needed). Then, we review investments and debt. If debt payoff should be a large part of their goals, we allocate money for that in the plan.

Next, we establish our asset accumulation goals. Since we’ve already discovered how much money we have to work with, we now need to find each dollar a home.

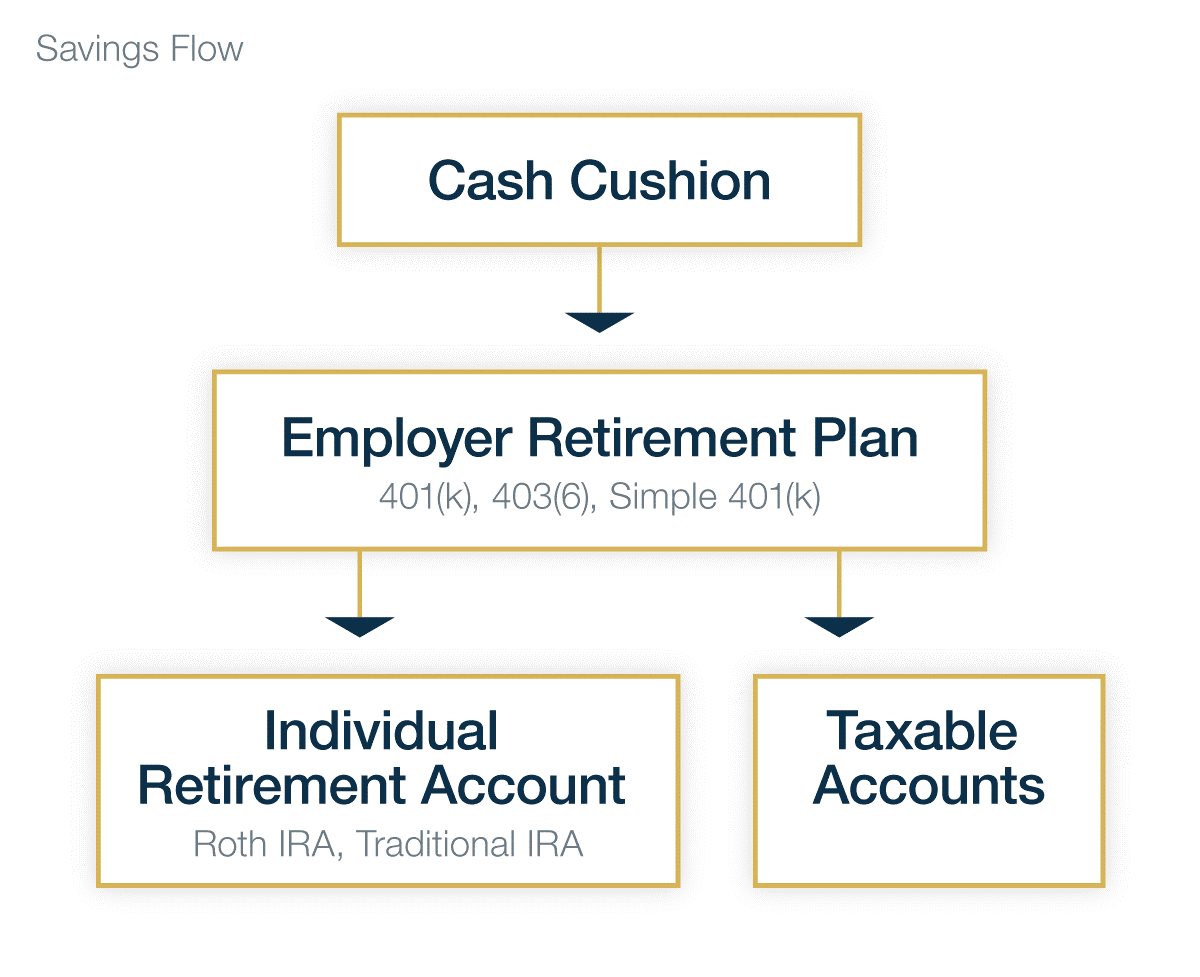

Imagine you have multiple buckets of water to fill. The first is your savings account or cash cushion, which must be filled to the brim. Then comes the retirement plan at work, which should be filled until you reach the employer match. Next, it’s time to look at your individual goals and utilize a spectrum of investment accounts, retirement included.

Using this hierarchy, we’re ready to begin selecting the appropriate investment vehicles, which boils down to a four-step process.

Step 1: Cash Cushion

The first account you fund is your personal savings, which I like to call your cash cushion. This may start as small as $1,000 or be as large as $50,000. This cushion is very specific to an individual’s needs and there is no general amount to target. This unique need depends on many factors, including household income, job security, individual tolerance for risk, personal health and goals.

Your cash cushion should be allocated for the following cracks in cash flow:

- Potential job loss

- Insurance deductibles

- Health issues

- Preparation for the unforeseen

Step 2: Retirement

Once the cash cushion is set, leftover money flows to investment accounts for retirement. Saving into various types of accounts is important, but some may be filled before others depending on cash flow. The types of accounts you’ll utilize are:

- Workplace Retirement Plan: 401(k), 403(b), SIMPLE 401(k)

- The minimum contribution should be made until the employer match is reached. Likewise, pay attention to when employer contributed funds becomes yours or are vested.

- Once the match is reached, leftover funds can flow to taxable accounts to make them more available.

- Traditional IRA

- If your employer does not match contributions, a Traditional IRA may be used as an initial retirement account.

- Before contributing additional funds to this plan, you’ll want to first reach the employer retirement plan maximum and fund taxable accounts.

- Roth IRA

- A Roth IRA may also be used as an initial retirement account if your employer does not match contributions.

- If income allows and your employer retirement account does not provide a Roth option, this is the account you’ll want to max out first.

Step 3: Unlocked Funds

This step differentiates between having your savings in a tax-deferred account vs. having your money locked away in retirement. Many advisors follow a belief that the only way we can save is a “set it and forget it” mentality. I teach my clients a different approach.

I trust that my clients have self-control, and I also want them to plan beyond retirement. Funding a taxable account with extra dollars instead of automatically maxing a plan through your employer creates a separate investment account that can still be used for retirement along with other goals.

Once your employer match is reached, a portion of your savings should be allocated in a taxable account to reach intermediate and long-term goals. A great motivator is to attach a financial goal to this account. This can be many goals, including:

- Buying property

- Traveling

- Leaving a legacy

- Retiring comfortably

Step 4: Additional Funds

Now that you’ve successfully funded your cash cushion, received the employer match in retirement and established taxable accounts to pursue your goals, it’s time to pat yourself on the back. You’ve established the skeleton of accounts needed for success. The next step is to ask yourself one question: What about additional funds?

The first option is to go back to your retirement plan at work and save until you reach the maximum contribution. Once you reach the contribution limit at work, you can fund a traditional IRA. Anyone can contribute to an IRA, but you may not be able to deduct it. Reserve this question for your CPA or tax professional.

If you are a business owner or highly compensated employee, you may also look into deferred compensation plans or other savings vehicles while continuing to fund taxable accounts.

This system allows you to utilize various types of accounts to meet specific goals at specific times. It maximizes your assets in case of a sudden financial bind, early or planned retirement, and beyond.

How do you figure out which flow is right for you? Sit down with a trusted advisor and create a plan for your future.

(This article is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate tax professional should be sought.)